In the past few years the IT sector has been characterized by continuously high growth and has frequently surpassed even its own forecasts. However, this trend failed to continue to the same extent in 2019 – and 2020, too, has been a challenging year due to the influence of Covid-19. The market for IT services must react to these unusual times, but can emerge stronger from this difficult phase – as shown by this study.

The IT sector is also showing growth in 2020, even if less than forecast

2020 follow-up study: The new Lünendonk study “The market for IT consultancy and IT services in Germany”

IT service providers are able to open up new areas

In 2019 the IT sector boom, which has in particular in the last few years demonstrated enormous growth, suffered a small setback. IT consultancy and IT services grew by only 7.8%. This is significantly less than previous years and diverges strongly from the forecasts of IT service providers. There are many reasons for this: trade tensions, structural crises and cautious investment amounts. As a result, the tense economic situation led to a focus on basic operations and existing systems.

Mario Zillmann from Lünendonk sees the current situation as an opportunity which can be tackled with boldness. Topics such as digital sales channels, digital workplaces and the increased use of cloud solutions can now finally be promoted.

The study looks at:

- Actual figures for development in the IT services sector and forecasts

- Theories on the future of the sector

- The Lünendonk lists of the leading IT consultancies, the leading medium-sized IT consultancies and the leading IT service companies in Germany

- Discussion and interviews with experts

- Assessments and comments on the topic of Covid-19

")

Here you can find everything you need to know about the changes to the IT service provider market.

The study was carried out by market research and consultancy firm Lünendonk & Hossenfelder GmbH. 76 IT service companies operating in Germany were surveyed between February and April 2020.

The full results of the study as well as further assessments by and interviews with various experts can be read in the complete study. This is available free of charge. What follows is a brief summary of some important findings and figures.

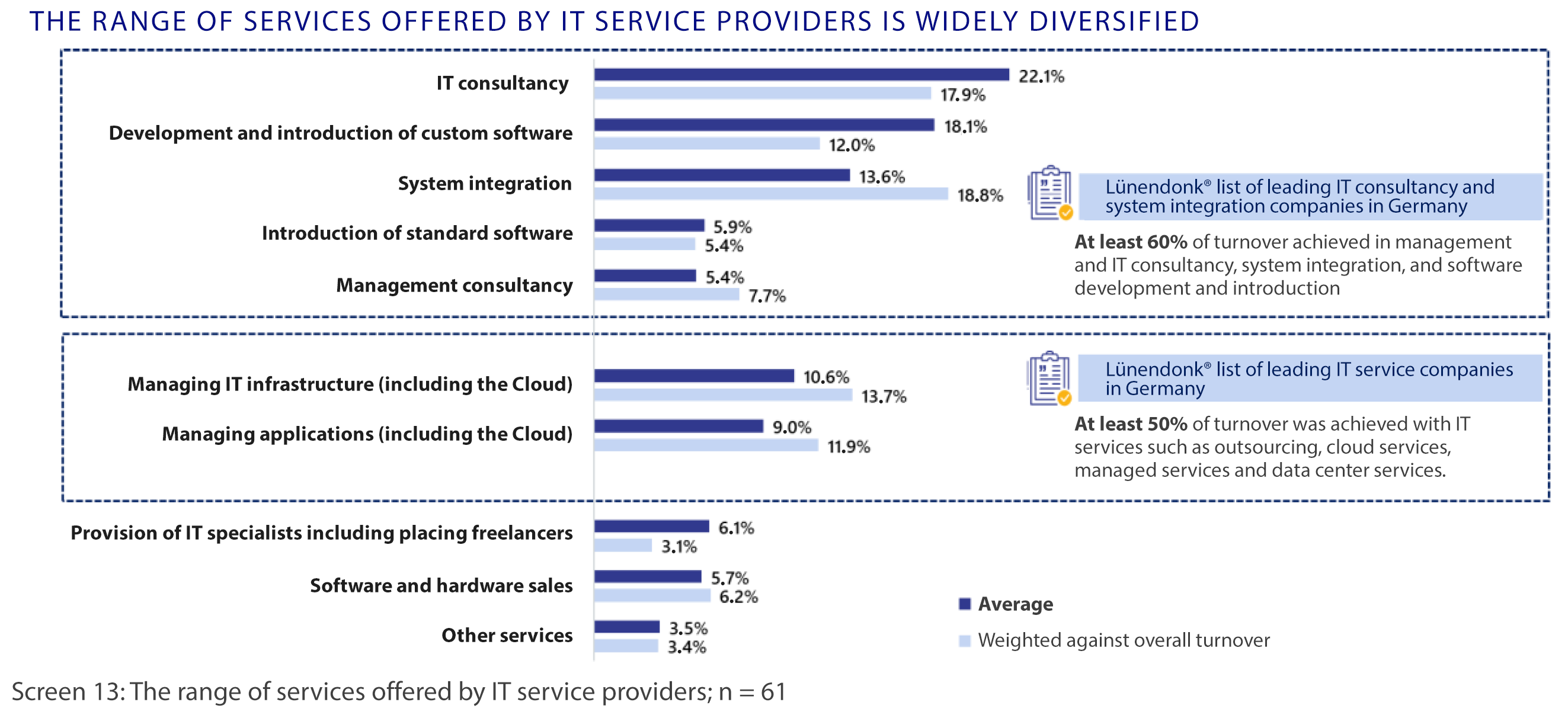

IT consultancy remains at the top of the range of services

The study looked at ten service categories and their proportion of the company’s turnover, with a focus on IT consultancy and system integration. It is hardly surprising to find IT consultancy at the peak of this assessment with a statistical average of 22.1%. Following closely in second place is the development and introduction of custom software with 18.1%. This is an increase of approx. 5% in comparison to the figures from five years ago. Standard software introduction was surveyed separately (5.9%) for a more precise differentiation.

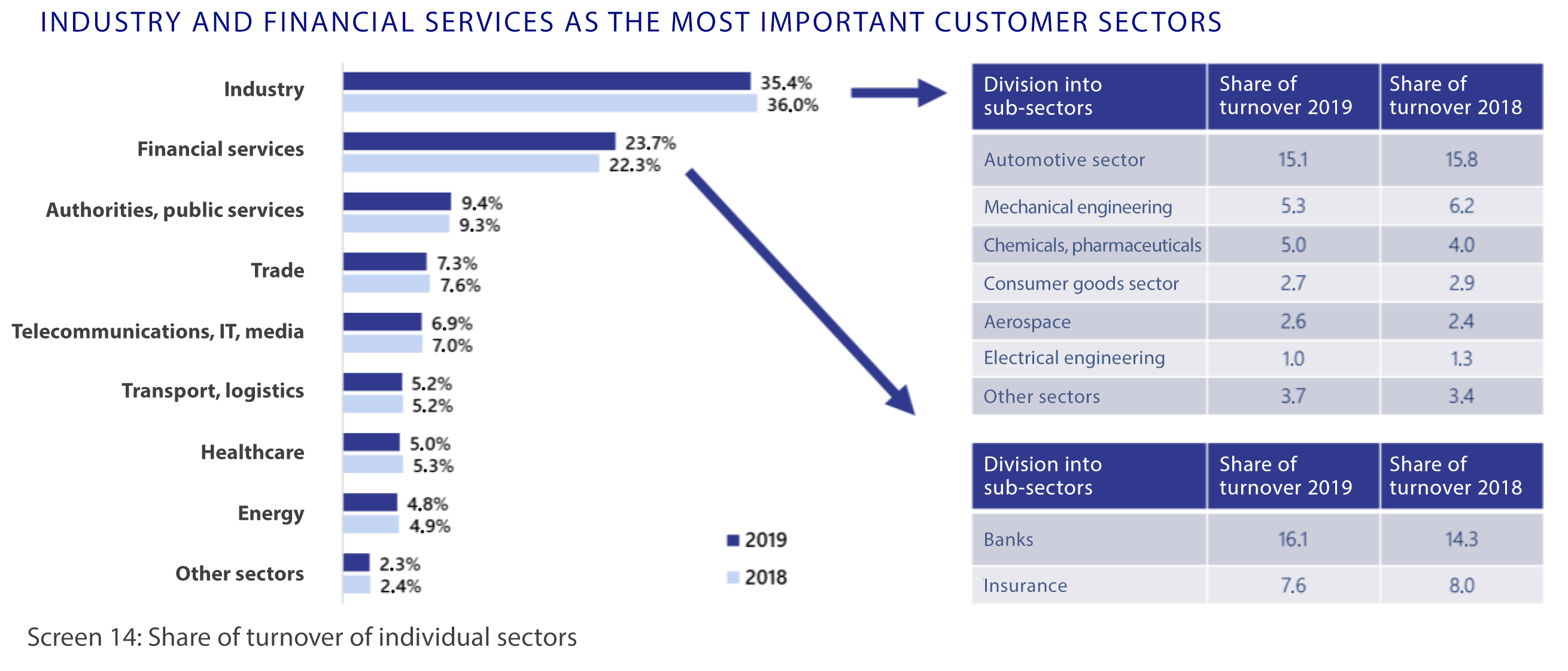

The most important sector for IT service providers: industry

Which sectors do the customers of IT consultancies come from? The results of the study confirmed the figures from the previous year: around 35% of customers come from the industrial sector (2018: 36%). Within the industrial sector, the areas of pharmaceuticals and chemicals grew by 1%, whilst the share of companies in plant and mechanical engineering, for example, has decreased. It is no coincidence that industrial companies continue to be so significantly ahead of financial service providers and public authorities. There is currently enormous pressure towards further digitalization measures and as a result towards more efficient processes and lower costs.

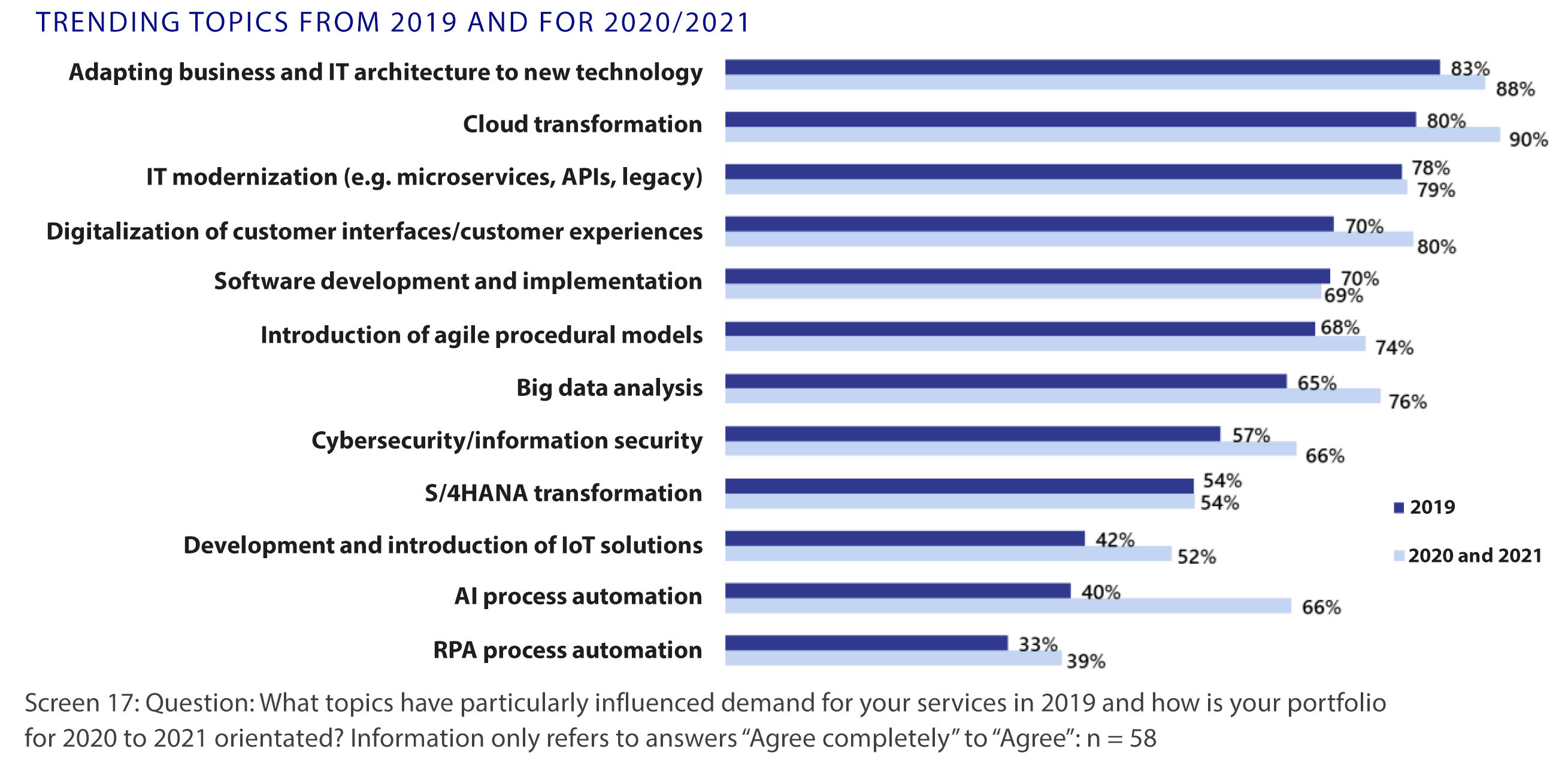

Everyone’s talking about the Cloud – but customers are preoccupied with yet other trends

In order to survive in the IT market, you need to know what the customer is interested in and which topics and trends are the most in demand. The IT service providers surveyed said that demand for providing cloud migration services had significantly increased by 80%. As such, it is expected that cloud projects will make up 15.7% of turnover in 2020. Similar figures were observed regarding demand for adapting business and IT architecture to new technology (83%) and IT modernization (78%).

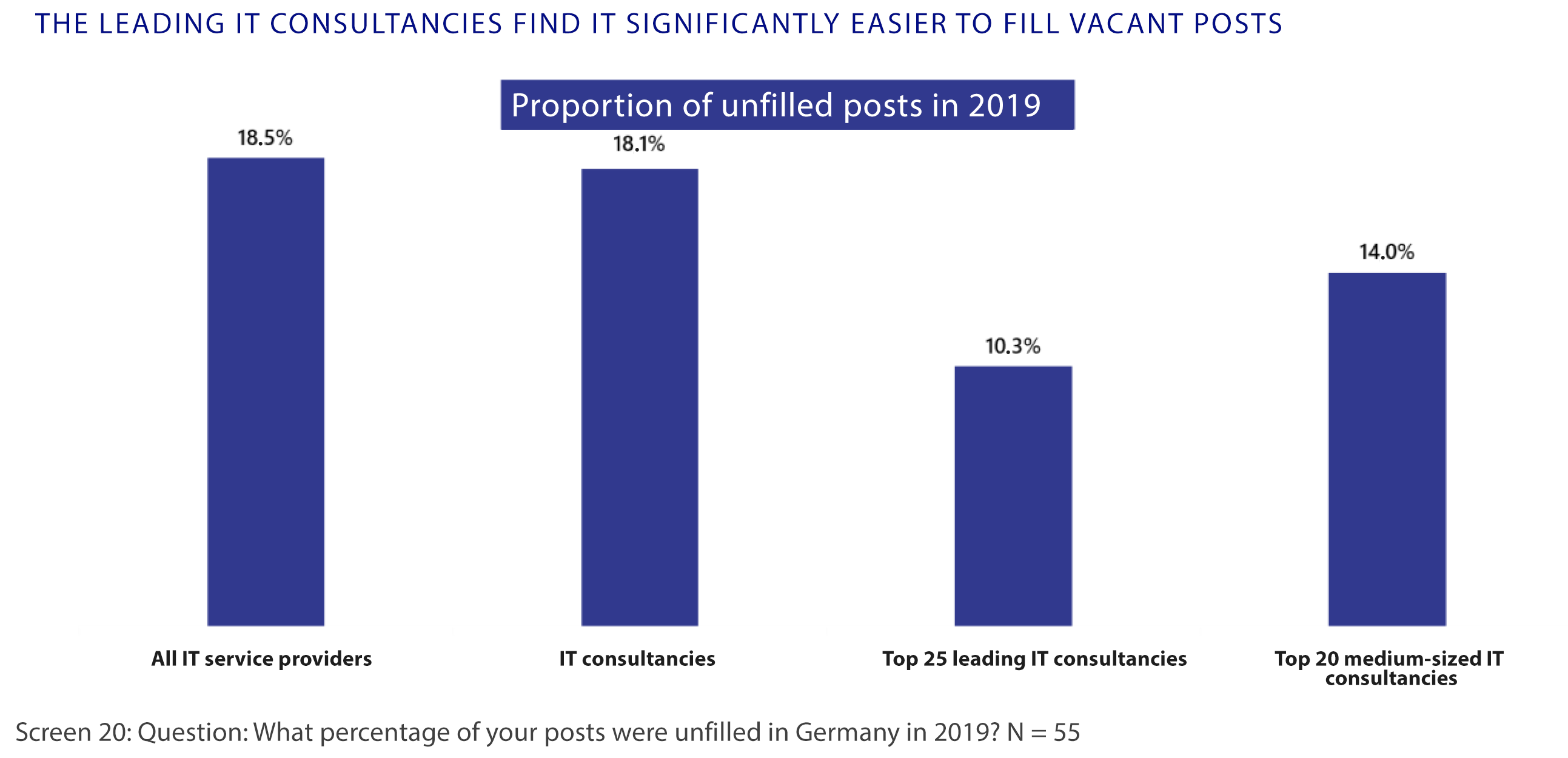

The personnel situation remains fraught

It has been clear for several years that demand for IT services will only be satisfied long-term with the necessary specialist personnel. Therefore, the affected companies have also supplemented the number of employees. The workforce grew by 6.3% across all service providers surveyed. However, this does not mean that this growth is enough. Despite increasing employee numbers, an average of 18.5% of advertised vacancies remain unfilled. This, among other things, is one of the reasons that 12.2% of project inquires have to be turned down.

Further study results on this and other topics can be found in the 2020 Lünendonk study: “The market for IT consultancy and IT services in Germany” (only available in German). This can be downloaded here in PDF format free of charge.